The Mason Jar Retirement Plan That Actually Beat the Stock Market

Every financial advisor has heard the story: some elderly client's parent kept thousands of dollars stuffed in mason jars buried in the backyard, missing out on decades of compound investment growth. The moral is always the same — don't be like grandma, trust the markets.

But what if grandma was actually the smart one?

The Financial Sophistication Hidden in Simple Glass

Between 1929 and 1942, millions of American families made a calculated decision to keep significant portions of their wealth in physical cash, often stored in mason jars and hidden around their properties. Modern finance dismisses this as Depression-era paranoia, but the math tells a different story.

Consider the Miller family of rural Ohio. In 1930, patriarch James Miller pulled $2,000 from his failing bank account — roughly $35,000 in today's money — and buried it in mason jars around his 40-acre farm. His neighbors called him crazy for abandoning potential investment returns.

Photo: James Miller, via brotherjamesmiller.org

Photo: James Miller, via brotherjamesmiller.org

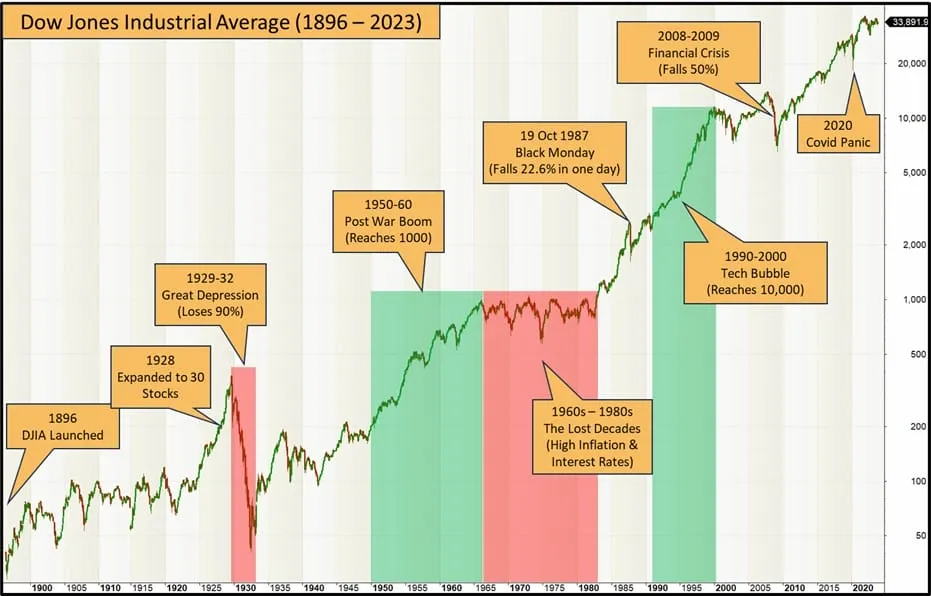

By 1942, the Dow Jones Industrial Average had fallen 48% from its 1929 peak and wouldn't recover to 1929 levels until 1954. Meanwhile, the Miller family's mason jar money retained 100% of its nominal value and actually gained purchasing power as deflation made goods cheaper throughout the 1930s.

Photo: Dow Jones Industrial Average, via enlightenedstocktrading.com

Photo: Dow Jones Industrial Average, via enlightenedstocktrading.com

The Three-Part Strategy Nobody Talks About

What looks like simple hoarding was actually a sophisticated three-pronged approach to capital preservation that most modern investors never consider.

Liquidity Insurance: Mason jar money was immediately accessible without paperwork, fees, or institutional approval. When banks failed or imposed withdrawal limits, families with buried cash could continue operating normally.

During the 1933 "bank holiday" when President Roosevelt temporarily closed all U.S. banks, families with mason jar reserves were the only ones with spending power. They could buy distressed assets from desperate neighbors, maintain their farms and businesses, and survive economic disruption that destroyed overleveraged competitors.

Deflation Hedging: While investors focused on missing out on stock gains, mason jar families were positioned to benefit from falling prices. Between 1929 and 1933, consumer prices fell 25%. A dollar buried in 1929 could buy $1.25 worth of goods by 1933.

This wasn't accidental. Many Depression-era families had lived through the deflationary periods of the 1890s and understood that cash gains value when prices fall — something modern investors, conditioned by decades of inflation, rarely consider.

Counterparty Risk Elimination: Money in mason jars had no counterparty risk. It couldn't be lost through bank failures, broker fraud, or institutional collapse. Given that nearly 10,000 banks failed during the 1930s, this wasn't paranoia — it was prudent risk management.

The Psychology That Wall Street Misunderstands

Modern financial planning assumes that investment growth should be the primary goal, with liquidity and capital preservation as secondary considerations. Mason jar families reversed these priorities, and their reasoning was more sophisticated than most advisors realize.

They understood that in unstable economic environments, the ability to act quickly matters more than optimal returns. Having cash available to buy a foreclosed farm at 30 cents on the dollar was more valuable than earning 3% annual returns on money locked in failed financial institutions.

They also recognized that financial markets and physical assets operate on different timescales. While stock prices fluctuate daily, farmland, homes, and businesses change hands infrequently and often at distressed prices during economic crises. Patient cash holders could time these purchases in ways that institutional investors couldn't.

When "Primitive" Beats Professional

Compare the mason jar strategy to professional portfolio management during the same period. The typical "sophisticated" investor of 1929 held a diversified portfolio of stocks and bonds, often purchased on margin and managed by professional brokers.

By 1932, this sophisticated approach had destroyed 89% of stock market value. Even conservative bond portfolios suffered as corporate and municipal defaults soared. Professional money managers, constrained by institutional requirements and client expectations, couldn't adapt quickly enough to protect capital.

Meanwhile, families with mason jar money were buying up distressed assets at fire-sale prices. They acquired farms, businesses, and real estate that would generate wealth for generations — purchases that were only possible because they had maintained cash liquidity while others trusted financial markets.

The Modern Lessons Nobody Wants to Learn

The mason jar strategy contained insights about money management that remain relevant today, even if the specific tactics seem outdated.

Emergency Liquidity Beats Emergency Credit: Mason jar families understood that borrowed money isn't the same as owned money. Modern families often rely on credit lines for emergencies, but credit disappears precisely when you need it most — during personal or economic crises.

Deflation Protection Still Matters: While inflation has dominated American economic experience since World War II, deflationary periods remain possible. Japan experienced deflation for nearly two decades after 1990. During deflationary periods, cash outperforms almost every other asset class.

Institutional Risk Is Real Risk: The 2008 financial crisis reminded Americans that trusted institutions can fail overnight. While FDIC insurance now protects bank deposits, it doesn't protect investment accounts, and insurance itself depends on government solvency.

The Updated Mason Jar Strategy

Modern families can't literally bury cash in mason jars — inflation makes long-term cash holding impractical, and electronic payments make physical cash less useful. But the underlying principles remain sound.

The modern equivalent might include:

- Maintaining larger cash reserves than financial advisors typically recommend

- Keeping some wealth in physical assets that retain value independent of financial markets

- Prioritizing liquidity and capital preservation over maximum returns

- Understanding that the best investment opportunities often appear during the worst economic conditions

What Grandma Knew That Wall Street Forgot

Those Depression-era families burying money in mason jars understood something that modern finance has largely forgotten: wealth preservation isn't just about maximizing returns — it's about maintaining financial flexibility in an unpredictable world.

They knew that the best investment strategy is worthless if you can't access your money when you need it most. They understood that cash has option value — it gives you the ability to act when others can't.

Most importantly, they recognized that financial markets exist to serve real economic activity, not the other way around. Their mason jar money wasn't "sitting idle" — it was waiting for the right opportunity to deploy into productive assets at attractive prices.

The next time a financial advisor mocks the idea of keeping money in mason jars, remember: those jars contained more than cash. They held a philosophy about money that prioritized security over speculation, liquidity over leverage, and patience over performance.

In an era of financial complexity and institutional fragility, maybe it's time to rediscover some of that mason jar wisdom.